ICSI - WIRC FOCUS

Vol. XXX • No. 11 •Nov 2013

Chairman’s Blog

CHOICE, not CIRCUMSTANCES, determines your SUCCESS.

- Anonymous

CHOICE, not CIRCUMSTANCES, determines your SUCCESS.

- Anonymous

My Dear Professional Friends,

Greetings

I am extremely delighted to share with you that at the 41st National Convention of the ICSI held during 7-9 November 2013 at Hotel ITC Grand Chola, Chennai, Western India Regional Council was declared as the BEST REGIONAL COUNCIL for the year 2012. The various new initiatives and activities/programs undertaken under the Chairmanship of the then Chairman, CS Mahavir Lunawat have brought this laurel to the WIRC for the first time. I was privileged to be member of the team lead by CS Mahavir Lunawat. The cooperation and active participation of all the members and all the Chapters of the Region also contributed in this achievement. On behalf of WIRC, I extend my heartiest congratulations and also gratitude to all the members and chapters on this first-ever achievement. I was also fortunate to receive the Award along with CS Mahavir Lunawat, CS Ragini Chokshi, Vice-Chairperson, CS Sanjay Gupta, Treasurer in presence of CS S.N. Ananthasubramanian, President, CS B. Narasimhan, CS Umesh Ved, CS Vikas Khare and CS Atul Mehta.

At this moment, I also have to inform you that Pune Chapter of WIRC has been declared as the Best Chapter for the year 2012, which has added one more feather to the glory of ICSI-WIRC. I compliment CS Pawan Chandak, the then Chairman and his team for this achievement.

On 19th October 2013, a cultural evening was organized at Mumbai to celebrate the 42nd Foundation Day of ICSI-WIRC. Our members and students participated and performed at the program. I am thankful to CS Ajay Kumar and CS Shailesh Karande for conceptualizing and arranging the mimicry and musical show. I am thankful to all the members and students who contributed / performed in the show.

The ICSI-WIRC released one more publication on “Practical Aspects of Foreign Direct Investments” at Full day program on Foreign Direct Investments held at Hotel Krishna Palace, Mumbai on 23rd November 2013. I am thankful to CS A. Sekhar and CA Sudha G. Bhushan, who is also a member of ICSI, both of whom agreed to spare their valuable time for this effort despite their other professional engagements, for authoring the publication. I am proud to share that this is the 4th Publication of ICSI-WIRC during the calendar year 2013. I thank CS Prakash Pandya, for his continuous and untiring efforts in bringing out the publications.

As always, before concluding, I again appeal the members to join COMPANY SECRETARIES BENEVOLENT FUND

With Warm Regards,

CS Hitesh Buch

Chairman

ICSI-WIRC

Mumbai, 12th November 2013

Editorial Board

Photo Feature

Checklist on Diligence Report – Lending under Consortium Arrangement / Multiple Banking Arrangements under the New Companies Act, 2013

Introduction

Introduction

The Reserve Bank of India (RBI) vide its notification no RBI/2008- 2009/183 DBOD No. BP. BC.46/ 08.12.001/2008-09 dated 19/09/2008 has advised the Scheduled Commercial bank (excluding Regional Rural Banks and Local Area banks) to obtain regular certification ( Diligence report) by qualified professional, preferably a Company Secretary, regarding compliance of various statutory prescriptions that are in vogue as per specimen given in the notification.

This notification had clarified that Central Vigilance Commission,Government of India, in the light of frauds involving consortium/multiple banking arrangements which have taken place recently, has expressed concerns on the working of Consortium Lending and Multiple Banking Arrangements in the banking system.

The Commission has attributed the incidence of frauds mainly to the lack of effective sharing of information about the credit history and the conduct of the account of the borrowers among various banks.

Looking to above, the RBI has decided to obtain regular certification by qualified a Company Secretary in practice (PCS) .

As the Company Secretary is qualified professional qualification & he has expert knowledge of various laws applicable to the Companies registered under the Companies Act, 2013.

The appointment of practicing company secretary (PCS),remuneration and other requirements are mutually decided between PCS and Company.

As per notification, this report are being preparing for half yearly basis.

This notification shall be applicable to borrowers availing sanctioned credit limits of Rs.5.00 crore and above or wherever, it is in their knowledge that their borrowers are availing credit facilities from other banks.

Now the both houses have passed the Companies bill, 2013 and it has also become Companies Act, 2013 on 30th August after the assent of the President of India.

After the passing of Companies Act, 2013 and all formalities have also changed and enlarged with respect to the Checklist on Diligence Report – Lending under Consortium Arrangement / Multiple Banking Arrangements

The PCS needs to check and report on the compliance of the following requirements.

1) Ensure whether the Company has maintained proper books of account, register, records and papers as per section 128 of Companies Act 2013 and the rules made there under, the provisions of various statutes, wherever applicable.

It can be further ascertained by followings

• To call a list of books of accounts maintained by the company

• As per Companies Act, 2013, books of account can be maintained in electronic mode.

• To check for situation of registered office of the company where the proper books of account to be maintained as per 128(1) of the Companies Act, 2013.

• If the company is not maintained the books of account at the registered office of the company and maintained other than registered office, then PCS has to check the relevant form filed to the concerned Registrar of Companies.

• To check other statutory records like Minutes of Board Meeting including its committee, Minutes of General Meeting, Register of members,Register of charges, Register of Directors, Register of Directors shareholding,Register of share transfer, Register of Investment, Register of share application and share allotment,Register of Contracts and Annual Return and any other return filed to stock exchanges, where the shares of the company is listed.

2) Ensure whether the Company is listed on the recognized stock exchange and to check compliance as per listing agreement executed with the stock exchanges and further to check the timely payment of listing fees.

3) Ensure whether the company has filed DIN 3 for all its directors or not and if not, report pending status DIN. To check Register of Directors and key managerial personnel maintained under section 170 of the Companies Act, 2013. For Managing Director, to check compliance as per section 196 & 197 schedule V to the Companies Act, 2013.

4) Ensure that directors of the company are not disqualified as per section 164 of the Act. For safe guard, obtain an undertaking from the director concerned for this purpose.

5) Ensure that list of shareholding pattern is tallied with the Register of Member and to also check from last annual return flied to ROC & return filed to stock exchanges, note if there is any variation.

6) Ensure that the company has complied provisions of Companies Act, 2013 for alteration in the Memorandum & Articles of Association.

To also check the company has communicated to concerned stock exchanges for its alteration as per listing agreement.

To further check such intimation to be given to consortium bankers, as per working capital agreement and term loan agreement if any.

7) Ensure that the company has complied the provision of under section 184,188, 189 & 190 of the companies Act, 2013 for the transactions with business entities in which directors are interested.

To call the list of business entities in which directors are interested. Alternately, it can also been checked online through MCA web site.

It can also be checked from the Auditors report in related party disclosures, Register of Directors & Register of Contracts.

8) Ensure that the company has complied the provision of under section 185 of the Companies Act, 2013 for loans to directors.

Please note that this section does not apply to Private Limited Company unless it is subsidiary of a public company but PCS has to report accordingly.

9) Ensure that the company has complied the provision of under section 186 of the Act for loans and investment or given guarantees to other business entities.

10) To report the summary of borrowings from Directors, members, Public, Financial institutions, banks and other banks.

• To report separately the list of borrowings from banks out side the consortium arrangements. Generally, the company has always has few transactions with them for purpose of the business.

To review the provisions of under section 180 & 181 of the Companies Act, 2013 and further the all borrowing are within the limit of borrowings limit are not.

If the company has taken the borrowing from public and it means all provisions of public deposits shall also be checked as per section 73 of the Companies Act, 2013 & rules made there under i.e. the Companies Public deposit rules.

11) Ensure that the Company has not defaulted in the repayment of any public deposits or unsecured loans and the Company or its Directors are not under the Defaulter's list of Reserve Bank of India or in the Specific Approval List of ECGC.

To check the name of company for the Defaulter's list of Reserve Bank of India from the list suit –filed accounts of defaulters from the web site of Credit Information Bureau (India) Limited (CIBIL). Please see web site of CIBIL i.e www.cibil.com under the clause “ suite filed cases.”

Alternately, the company’s bankers can also give this list.

12) Ensure that the Company has timely created, modified or satisfied charges on the assets of the company as per section 77, 79, 81 & 82 of the Companies Act, 2013.

Please also see of the Register of Charges maintained.

Please note that every company has to keep all copies of every instrument of charges at the registered office of the Company.

13) Ensure that the company has compiled the requirement of the Forex exposure and Overseas Borrowings.

Overseas Borrowings includes ECBs and details of external commercial borrowings (ECBs) to be checked very care fully.

External The Commercials Borrowings include bank loan, suppliers and buyers creditors, fixed and floating rate bonds (without convertibility) and borrowings from private sector window of multilateral financial institutions such International Finance Corporation, Euro Issues include convertibility bonds and GDRs.

In India, ECB are being permitted by the Government for providing an additional source of funds to Indian Corporate and PSUs for financing expansion of existing capacity and as well as for fresh investment, to augment there sources available domestically. ECBs can be used for any purpose (rupee related expenditure as well as imports) except for investment in stock market and speculation in real estate.

The Department of Economic Affairs, Ministry of Finance, Government of India with support of RBI, monitors and regulates Indian firms access to global capital markets. From time to time, they announce guidelines on policies and procedures for ECBs and EURO issues.

To focus the checking on ECBs in following manner;

• Eligibility criteria for accessing external markets

• The total volume of borrowings raised and their maturity structure

• End use of the funds raised.

Please also review the additional requirement of consortium banks / listing requirements / SEBI guidelines, if any.

14) Ensure that the company has properly issued, offered and allotted all the securities to the persons entitled thereto and has also issued letters, coupons, warrants and certificates thereof to the concerned persons and also redeemed its preference shares/debentures and bought back its shares (wherever applicable) in compliance with the specified procedures and within the stipulated time.

Please also check SEBI guide lines / listing requirements / provision of Memorandum & Articles of Association / Provisions of section related to issue of prospectus, allotment of securities/ securities issued on premium or discounts/ Bonus issue guide lines/ redemption of preference shares & debentures /shares allotted to employees / guidelines for issue of shares certificates / special provisions related debenture from u/s 71 the Companies Act, 2013 including their registration of charges.

15) Ensure that the company has full coverage of insurance for its all secured assets and all non secured assets.

• Please review list of insurance coverage with value of assets and sum insured.

• Please also review the Register of Fixed Assets maintained by the company.

• Please also review insurance claim pending / settled during the year under review.

• Please also check insurance coverage for building under constructions / machineries under installations.

• Please also review insurance coverage for domestic marine policy and export marine policy.

16) Ensure that the Company has complied with the terms and conditions, set forth by the lending institution at the time of availing the facility and also during the currency of the loan and has utilized the funds for the purposes for which these were borrowed.

PCS has to be checked very carefully with the followings;

• Utilization of short term working funds into long term purpose and vice versa

• Utilization of funds in the other assets for which the sanctioned not granted

• Transfer of funds into group companies / subsidiaries companies.

• Utilization of funds into long and short terms investment

• Transfer of funds into other banks (which is not member of consortium) without permission of consortium banks

• Utilization of funds for not the business of the company (for personal properties of the Directors)

The above transactions are only illustrative not exhaustive.

PCS has to call list of machines sanctioned from bank and check accordingly.

To check further:

• Financial transactions between group companies and subsidiaries companies

• Cash flow and fund flow of the company including group company/ subsidiary company

• To check General ledger trial balance / bank statement/ assets purchased during the year/ party ledgers and any accounts / books which is related for this purpose.

PCS may also check the other details for diversion & end use of the funds as per need.

17) Ensure that the Company has declared and paid dividends to its shareholders as per the provisions of the Companies Act, 2013.

Check the requirement of listing agreement / bank documents for working capital and term loans.

18) Ensure that the Company has paid all its statutory dues and that there are no arrears as per section 43 B of the Income tax, 1961. If the company has not paid the legal dues on time.

It has to be reported with amount of penalty and period of delay.

19) Ensure that the Company has complied with the applicable and mandatory Accounting Standards issued by the Institute of Chartered Accountants of India.

This is Directors responsibilities to comply the provisions as per section 134 of the Companies Act, 2013.

20) Ensure that the Company has credited and paid to the Investor Education and Protection Fund all the unpaid dividends and other amounts required to be so credited.

21) Ensure that the company has properly replied show cause notices received by the Company for alleged offences under the Act.

Ask to arrange a list of prosecutions initiated against or and also the fines and penalties or any other punishment imposed on the Company in such cases is be attached with report.

22) Ensure that the Company has complied with the various clauses of the Listing Agreement, if applicable.

23) Ensure that the Company has deposited both Employees' and Employer's contribution to Provident Fund with the prescribed authorities. Ensure that the payment has also been deposited as per Income Tax Act, 1961 and if not deposited as per Income tax, such expenditure shall not deductible from the Income as per Income tax. It shall be reported accordingly.

24) Appointment of Key Managerial person as per section 203 of the Companies Act, 2013

25) To check the provisions of independent directors separately

26) To check the provisions of audit committee and other various committee meeting with respect to formation and meeting procedures.

27) To check the provisions of officers who is in default.

28) To check the provisions of women directors, if any.

29) To check the provisions of applicability of Secretarial audit and cost audit, if any.

30) To review CSR activities, if any

Other Important points to be considered while checking and further reporting.

• To review last Audited Annual Report, Internal & Management Audit report & Secretarial compliance report / Legal Compliance Report / Cost Audit Report, Stock audit report if any

• To review all correspondences with Banks, financial intuitions regarding working capital facilities, term loan and other loans etc and may also review all correspondences from other legal authorities.

• To review all correspondences with ROC and stock exchanges

• To call a list of applicability of various laws as per requirement & need of business of the Company.

• The qualification / reservation or adverse remarks, if any, may be stated at the relevant places in the report, PCS has to quantify the full details of qualification / reservation or adverse remarks, if any.

• To review pending the legal proceedings, if any.

• PCS may obtain certified copies of the statements / papers / documents from the company’s directors.

• PCS may also review master data, list of companies in which director is interested through DIN and other data available on the MCA website( www.mca.gov.in) of the company including all other their group companies and subsidiary companies.

• Diligence Report (In Annexure III) shall be submitted to bank within time frame work decided by the bank.

Significance of Corporate Resolutions and Minutes

Introduction & Background

In today’s corporate era, corporate resolutions or minutes of meetings are crucial to the running of a Company or Corporation. Proper, timely corporate minutes help protect personal assets of owners and officers. The main advantage of corporate establishments is that the shareholders are mostly free from liabilities except for the equivalent of the money they have invested. To avoid crossing the line and maintain the veil that separates the investors from the business, the company should adopt measures of good governance and keep everything formal. A way to keep a company’s corporate veil is by keeping good corporate minutes and preparing them in good fashion. The company just needs to make an effort to start systematizing the process of generating corporate meeting minutes and resolutions to cover official company business.

In today’s corporate era, corporate resolutions or minutes of meetings are crucial to the running of a Company or Corporation. Proper, timely corporate minutes help protect personal assets of owners and officers. The main advantage of corporate establishments is that the shareholders are mostly free from liabilities except for the equivalent of the money they have invested. To avoid crossing the line and maintain the veil that separates the investors from the business, the company should adopt measures of good governance and keep everything formal. A way to keep a company’s corporate veil is by keeping good corporate minutes and preparing them in good fashion. The company just needs to make an effort to start systematizing the process of generating corporate meeting minutes and resolutions to cover official company business.

Provisions pertaining to the minutes of the meeting are covered under Section 193 to 196 of the Companies Act, 1956. Section 193 states that Minute of proceedings of general meetings and of Board and other meetings. Section 194 provides Minutes to be evidence. Section 195 states the Presumption to be drawn where minutes duly drawn and signed. Section 196 provide for inspection of minute’s book of general meeting.

Further, Companies Bill, 2012 passed by lok sabha also familiarized provisions pertaining to the Minutes as clauses 118 and 119 after some addition and modification to the existing Sections of the Companies Act, 1956.

Corporate resolutions include most formal actions and decisions approved by board of directors and also define which individuals are authorized to act on behalf of a Company or Corporation. There are multiple situations in which a specific resolution to cover a particular transaction. Corporate Resolutions record the major decisions taken by shareholders or board of directors during a meeting. Some Corporate Resolutions may be passed only by the Shareholders in the general meeting i. e. (a) Ordinary Resolutions (b) Special Resolutions (c) Resolutions requiring special notice; other Resolutions - only by the Board of Directors i. e. (a) Resolutions passed by simple majority (b) Resolutions passed by circulation (c) Resolutions passed with the consent of all directors present at the meeting.

CORPORATE RESOLUTIONS:

Definitions:

The term 'resolution' has not been defined in the Companies Act, 1956. Hence, taking the Dictionary meaning of the word ‘RESOLUTION’ is – ‘a formal proposal put before a public assembly or the formal determination of such proposal on any matter’.

A corporate resolution is a corporate action, sometimes in the form of a legal document that will be voted on or has been voted on at a meeting of the board of directors for a corporation. The resolution could also be in the form of a "corporate action" which has the same binding effect as an action taken at a duly called meeting. For a corporate action, if allowed by state law and by the bylaws of the corporation, the board of directors may use a written document to waive formal notice of a meeting and unanimously consent to a resolution.*

Types of Resolutions:

• Resolutions of the General meetings:

The manner of decision making by members in the general meeting of a company is to pass a formal special or ordinary resolution considering the requirements of the Companies Act, 1956, the Memorandum of Association and Articles of Association of the company. The following types of resolutions are required to be passed at a general meeting as per requirements of the provisions of the Companies Act, 1956.

(a) Ordinary Resolutions

(b) Special Resolutions

(c) Resolutions requiring special notice.

• Resolutions of the Board meetings:

Matters are generally decided at the Board meetings by way of formal resolution with simple majority of the directors present at the meeting. Resolutions can also be passed by circulation among the directors in accordance with the provisions of section 289 of the Companies Act, 1956. The following types of resolutions are generally passed by the Board of directors of a company.

(a) Resolutions passed by simple majority

(b) Resolutions passed by circulation

(c) Resolutions passed with the consent of all directors present at the meeting.

Importance of Corporate Resolutions:

A resolution that has been passed by the Board of Directors gives assurance to other parties in a transaction that the transaction was properly

authorized by the Board. A Director may be asked to show the resolution as proof in order to open a corporate bank account or conduct other

transactions on behalf of the Company. The resolution also indicates that the actions were taken on behalf of, and by, the Company, rather than

by a Director whose actions were not approved by the rest of the Board.

More formal than a verbal decision, a written and agreed upon corporate resolution can prevent later disputes between individual Directors or between the Board and a third party. All Resolutions passed by the Board of Directors of the Company should be kept for at least 8 years in the Company’s Corporate Minute Book. This written record can be useful in the event that the Board’s actions are challenged by shareholders or others.

Resolution goes with authority:

A Company is comprised of the members who contribute to the capital of the company, managed by the Directors who are the representatives of the members and activities of the company are regulated by the Government and its agencies to conform to the requirement set forth in the various statutes of which the Companies Act, 1956, is the principal regulatory force. The compliances of the regulatory inhibitions either requires certain action to be taken at the Board of Directors’ level or its committee or the exposition through Resolution, made at members’ meeting.

Resolution gives sanction to an act:

A ‘Resolution’ presupposes an assembly of either the Directors or the members who are to deal with the business and to record the consensus of the assembly. In the context of Company management, it is of either a Board Meeting or of a General Meeting of the members. The passing of a resolution should be construed as the manner in which a meeting formally acts expressing the interest and purpose of the meeting, and if it is a meeting of members, it means the will of the company, and if it is a meeting of the Board of Directors, it means the exposition of the intent of the executive action initiated or to be subject to the limiting and regulatory force of the different statutes.

Recorded resolution is evidence:

A resolution is a decision or an exposition of opinion or consensus of a proposal submitted before a meeting. A resolution is entered in the minutes of the particular meeting, which represent the record of proceeding of that meeting and the same can be presented as evidence to the court of law or other requisite authority.

CORPORATE MINUTES:

Definitions:

All issues discussed at a board meeting are included in the meeting's minutes. The minutes are recorded by the secretary of the board. They include all motions made and any resolutions discussed.

Permanent, formal and detailed although not verbatim, record of business transacted, and resolutions adopted, a firm's official meetings such as board of directors, manager's, and annual general meeting (AGM). Once written up or typed in a minute book and approved at the next meeting, the minutes are accepted as a true representation of the proceedings they record and can be used as prima facie evidence in legal matters.*

Importance of Minutes:

Forming a corporation is an important and sometimes exhausting task. Typically, after the new entity is established and the initial shares sold to stockholders, the owners take a deep breath and get back to doing what they do best in running the day-to-day business operations.

Unfortunately, as a result, the owners often put off dealing with many tasks necessary to running their new corporate entity.

Ignoring the care and feeding of your corporate legal entity is foolhardy. That's because failure to properly document and support important tax decisions and elections can result in a loss of crucial tax benefits. Even worse, the fact that you have ignored your own corporate existence may result in its being similarly disregarded by the courts, with the risk that you may be held personally liable for corporate debts. And, of course, as time passes and memories fade, if there is no written record of important decisions, directors or shareholders may forget who agreed to what and under what circumstances. This can lead to controversy and dissension, even in the ranks of a closely held corporation.

Fortunately, the regular structured use of written minutes and resolutions, which record all important corporate decisions and the votes taken to approve them, helps greatly to defuse all of these problems. Quite simply, your first and best line of defense against losing the protection of your corporate status while helping to ensure continued harmony among your directors and shareholders is to document important corporate decisions by preparing and maintaining adequate corporate records.

The good news is that you don't need to document routine business decisions -- only those that require formal board of directors' or shareholders' approval. In other words, you are not required to clutter up your corporate records book with day-to-day business records, such as those for purchasing supplies or products, hiring or firing low- or midlevel employees, deciding to launch new services or products, or any of the host of other ongoing business decisions.

But key legal, tax, and financial decisions absolutely should be acted on by your board of directors, and occasionally your shareholders. What kinds of decisions should be considered key? The proceedings of annual meetings of directors and shareholders, the issuance of stock to new or existing shareholders, the purchase of real property, the approval of a long-term lease, the authorization of a significant loan amount or substantial line of credit, the adoption of a stock option or retirement plan, and the making of important federal or state tax elections - these, and other key decisions, should be made by your board of directors or shareholders and backed with corporate paperwork. That way, you'll have solid documentation in the event that key decisions are questioned or reviewed later by corporate directors, shareholders, creditors, the courts.

Why bother to prepare minutes of meetings or written consents for key corporate decisions? Here are a few excellent reasons:

• Annual corporate meetings normally are required under state law. If you fail to pay at least minimal attention to these ongoing legal formalities, you may lose the limited liability protection of your corporate status.

• Your legal paperwork provides a record of important corporate transactions. This “paper trail" can be important if disputes arise. You can use this paper trail to show your directors, shareholders, creditors, suppliers, the Indian revenue service (IRS), and the courts that you acted appropriately and in compliance with applicable laws, regulations, or other legal requirements.

• Formally documenting key corporate actions is a fail-safe way of keeping shareholders informed of major corporate decisions.

• Directors of small corporations commonly approve business transactions in which they have a material financial interest. Your minutes or consent forms can help prevent legal problems by proving that these self-interested decisions were arrived at fairly, after full disclosure to the board and shareholders.

• Banks, trusts, escrow and title companies, property management companies, and other institutions often ask corporations to submit a copy of a board or shareholder resolution approving the transaction that is being undertaken, such as a loan, purchase, or rental of property.

Should reasons for decisions be recorded?

With the focus on accountability in the current regulatory and corporate governance environment, some commentators suggest as advisable the inclusion of broad reasons for decisions in the minutes. A brief outline of factors material to the decision, any dissenting views and the amount of time spent on discussion may help to establish that directors have exercised proper care and diligence in their decision making. Recording the length of time spent on a discussion can denote the relative importance of a matter to a board meeting, reinforcing that directors have given it due consideration.

Can minutes be used in court as evidence?

Minutes can be used as evidence. The minutes are not conclusive evidence of what happened at a directors meeting. It is evidence ‘unless the contrary is proved. For the presumption to apply there must be strict compliance with the one month limit.

Section 194 of the Indian Companies Act, 1956 provides that minutes of meeting kept in accordance with the Provisions of Section 193 shall be evidence of the proceedings recorded therein (the same provision also appears in Clause 118 (7) of the Companies Bill, 2012 passed by lok sabha).

Section 251A (6) of the Australian Corporations Act, 2001 provides that ‘A minute that is so recorded and signed is evidence of the proceeding, resolution or declaration to which it relates, unless the contrary is proved’.

Section 249 (4) of United Kingdom Companies Act, 1956 provide that Minutes recorded in accordance with section 248 of the Act, if purporting to be authenticated by the chairman of the meeting or by the chairman of the next directors' meeting, are evidence of the proceedings at the meeting.

Should Directors make their own notes of Board Meetings?

There is no legal obligation on directors to take personal notes. The responsibility for record keeping lies solely with the organization. It is unlikely that a court would view the absence of director’s notes as a sign that a director has not fulfilled his/ her duties.

Like minutes, directors’ notes can be requisitioned as evidence in court. This might be helpful if the notes show that the director has adequately informed him/ herself, questioned appropriately and used proper care and diligence. However, taking notes can create risk – ambiguous, inconsistent or incomplete records can be used against a director.

Boards have a responsibility to properly evaluate the minutes circulated after meetings. Directors may want to take notes during the meeting to refresh their memory when the minutes are circulated. They should request additions, clarifications or corrections where necessary. After the minutes are signed, there is no real reason to retain any notes.

When should minutes of the board meeting be signed and confirmed?

As per the clarification issued by DCA*, it is not obligatory to wait for the next Board meeting in order to have the minutes signed of the meeting already held. The chairman of the meeting at any time may sign such minutes before the next Board meeting is held.

A confirmation of minutes of a meeting at the next meeting is not contemplated under the law. [Department of Company Affairs’ (DCA) Circular No. 8/2 Miscellaneous 75-CL-V, dated 5 May, 1975.] Recently the Department had an occasion to consider the question whether a chairman of one board meeting or a committee of the board should cause minutes of all proceedings of every meeting of its board within 30 days of the conclusion of every such meeting as per sub-section (1) of section 193, or whether it can be legally contended that the chairman of the next board meeting to be held within the meaning of section 285 of the Act, can validly sign such minutes.

Minutes must be signed latest on the date of the next succeeding meeting of the Board. It is not necessary that the minutes are signed by all the directors present at the meeting [Prafulla Kumar Rout v orient Engg. Works Pvt. Ltd. 91986) 60 COMP Cas 65 (Ori) but it is necessary to mention the names of the directors present.

Can action be initiated on any resolution on conclusion of the meeting?

Action on any resolution or any matter approved by the board at a meeting can be taken immediately on the conclusion of the meeting. It is not necessary to wait till the minutes are recorded, approved and adopted at the next meeting. The non-confirmation of minutes does not have any effect on the decision taken at the earlier meeting. [Kerala State Electricity Board V/s Hindustan Construction Co. Limited [2009] 91 SCL 183 (SC).]

How are minutes to be maintained?

The Department of Company Affairs has issued a number of circulars and clarifications from which it appears that the Department would have no objection if the minutes are kept in loose leaf typewritten form, provided certain precautions are taken. Binding up the loose leaves in books at reasonable intervals, say six months and communicated to the board at a meeting. There should be proper locking device to ensure security and control. The minute’s book is kept in a locker and made accessible only to the company secretary.

Should minutes be numbered?

The pages of the Minutes Book should be consecutively numbered. This is for obvious reasons for preventing interpolation, manipulation, fabrication and substitution.

How old minutes are to be maintained?

Minutes of all Meetings should be preserved permanently. Office copies of Notices, Agenda, Notes on Agenda and other related papers should be preserved in good order for as long as they remain current or for ten years, whichever is later, and may be destroyed thereafter under the authority of the Board.

Whether inspection can be conducted?

The Companies Act, 1956 has no express provision in relation to inspection of minutes books of Board meetings, the same shall be open for the inspection of auditors. The directors shall also be eligible to see these books.

Board Meeting through video conference as per General Circular No. 28/2011 dated May 20, 2011:

With intent to support the largely globalized corporate structure and enable them, the Ministry of Corporate Affairs vide General Circular No. 28/2011 dated May 20, 2011 has introduced the much awaited concept of enabling participation of Directors in the meetings of the Board/Committee of Directors through Video Conferencing. This stride towards e-governance is not only a move which will largely support green initiatives but also a big boon of big corporate houses and Multi-National companies which severely required this provision to enable active participation of their Board members being globally located in various Meetings.

Section 2,4,5,13,81 of the Information Technology Act, 2000 read with the relevant provisions of the Companies Act, 1956. While section 2 defines various legal terms related to Information Technology orientation, Section 4 provides for Legal recognition of electronic records, Section 5 provides for Legal recognition of digital signatures, Section 13 provides for Time and place of dispatch and receipt of electronic record and Section 81 provides for the Act to have overriding effect.

Recording of meetings through Video conferencing:

As a step towards good governance, the complete meeting should be recorded for a specified time frame. However the General Circular No. 28/2011 dated May 20, 2011 issued by Ministry of Corporate Affairs provides for Video recording of conclusion of the meeting wherein the Chairman announces the summary of the decisions of the meeting and the names of directors consenting or dissenting to those decisions for a period of one year from the conclusion of the meeting. These are required to be preserved by the company for one year from the conclusion of that meeting.

Minutes of the Board Meeting held through video conference:

As per the circular, draft minutes of the meeting needs to be circulated in soft copy not later than 7 (Seven) days of the meeting to the directors who attended the meeting to dispel all doubts about on matters taken up during the meeting. Thereafter, the minutes shall be entered in the minute books as prescribed under section 193 of the Companies Act, 1956. The minutes shall also disclose the particulars of the Directors who attended the meeting through electronic mode. In the minutes, chairman shall also confirm the mode of attendance of every director of the company during last three meetings whether personally or through electronic mode.

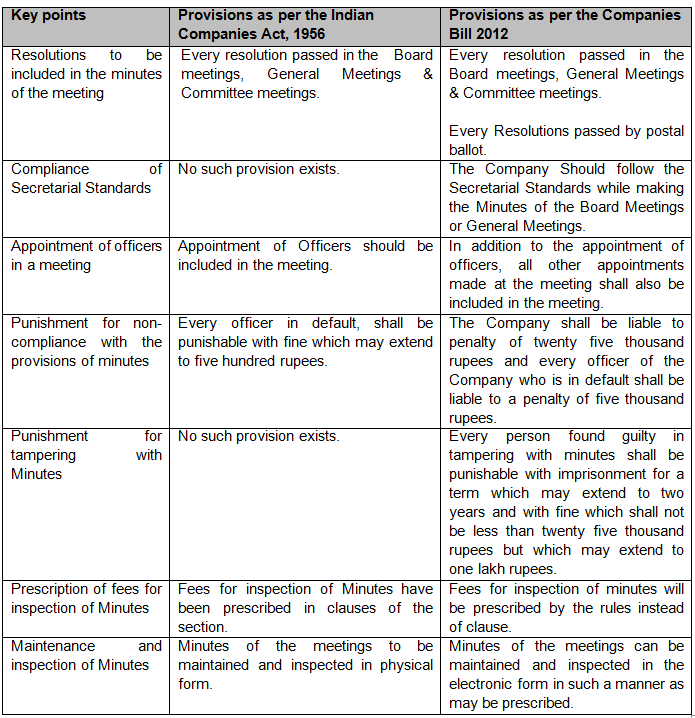

Comparison / highlights on the provisions of the concept of ‘Minutes’ as per the Companies Act, 1956 and Companies Bill 2012:

DIFFERENCE BETWEEN RESOLUTIONS AND MINUTES:

• A resolution is written documentation describing an action authorized by the board of directors of a Company. The minutes are a written document that describes items discussed by the directors during a board meeting, including actions taken and resolutions passed.

• A resolution is a written document that details an action or opinion adopted by a corporate board of directors. The minutes of a board meeting are another written document that describes all of the actions taken and any resolutions adopted by the board during a formal meeting.

• Resolution is specific to what has been resolved; minutes are typically a summary of a meeting that describes in general detail what occurred.

• A resolution is a written document that describes the actions taken by the board of directors of a Company. The minutes are a written document that describes actions taken and resolutions passed by the directors during a board meeting.

CASE LAWS:

James Hardie High Court Decision: Evidentiary Importance of Board Meeting Minutes:

On 3rd May, 2012 the High Court held that the seven non-executive directors of James Hardie Industries Limited (JHIL) had breached their duty to exercise care and diligence, by approving the release of a misleading announcement to the Australian Securities Exchange (ASX). This decision overturns the finding of the New South Wales (NSW) Court of Appeal. This decision has significant implications as to the evidentiary importance of board meeting minutes. The High Court held that inaccuracies in board meeting minutes and evidence that inferred the minutes were false did not counter the evidentiary value of the minutes as a primary record of what had occurred at the relevant meeting. [James Hardie Industries NV v ASIC [2010] NSWCA 332)]

Kerala State Electricity Board V/s Hindustan Construction Co. Limited [2009] 91 SCL 183 (SC):

In this case, the directors had resolved on few things in a particular meeting and in the next meeting they had 'not confirmed' the minutes of the previous meeting and therefore contending that the resolutions of the first meeting are not to be acted upon. In that context, the Supreme Court has stated that, “Confirmation of minutes of Board meeting or any committee meeting does not require confirmation in subsequent meeting. Non confirmation of minutes does not have any effect on the decision taken at the earlier meeting. When minutes of a meeting are placed before the next meeting the only thing that can be done is to see whether the decision taken at the earlier meeting has been properly recorded or not. Once a decision is duly taken it can only be changed by a substantive resolution properly adopted for such change.”

CONCLUSION:

Companies should urgently review the process by which they both keep and record minutes. The minutes should be prepared as soon as possible after a relevant meeting. They should be reviewed by the chairman, signed by the chairman and entered into the minute book. Where possible other director’s comments should be sought prior to signing. If they cannot be sought, then the same procedure should be used, but at the next directors meeting opportunity should be given for directors to comment on the minutes signed by the chairman. This way directors who believe that the minutes are inaccurately recorded, debate may place on record their views as to the minutes. The importance of recording the minutes promptly and preserving their evidentiary value cannot be overstated.

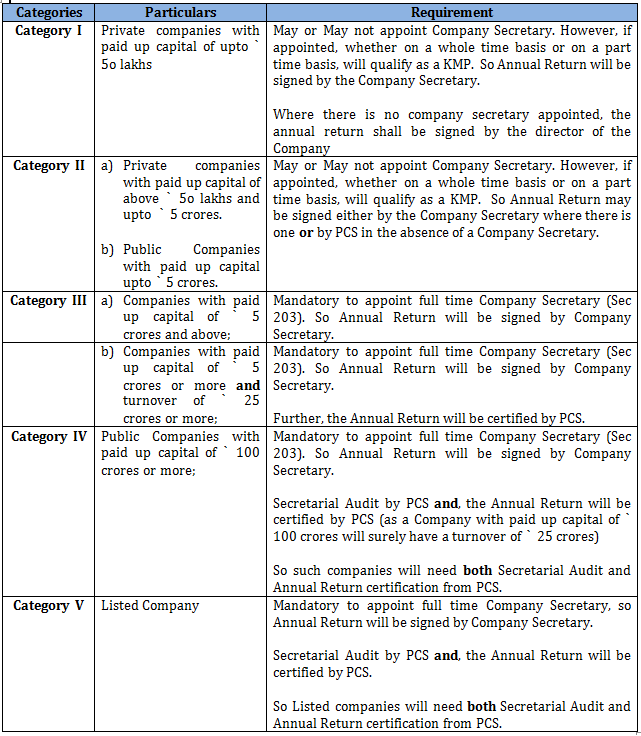

Look forward to heydays of CS Profession: Certification requirements under the new Act

There is enough buzz in the corporate world regarding the role of Practising Company Secretaries (PCS) under the Companies Act, 2013

(the Act, 2013). Professionals were worried inasmuch as the scope and position of a Company Secretary in employment seemed to have

increased, the role of PCS was a matter of concern when the corresponding section of 383A under the Companies Act, 1956 (the Act, 1956) was missing in the Act 2013. However, it seems that Act 2013 has widened the scope of services that a PCS can offer. One of such area is Annual Return to be filed by a Company under Section 92 of the Act, 2013

There is enough buzz in the corporate world regarding the role of Practising Company Secretaries (PCS) under the Companies Act, 2013

(the Act, 2013). Professionals were worried inasmuch as the scope and position of a Company Secretary in employment seemed to have

increased, the role of PCS was a matter of concern when the corresponding section of 383A under the Companies Act, 1956 (the Act, 1956) was missing in the Act 2013. However, it seems that Act 2013 has widened the scope of services that a PCS can offer. One of such area is Annual Return to be filed by a Company under Section 92 of the Act, 2013

Provisions of law

As per Section 92 of the Companies Act, 2013 (the Act, 2013), the Annual Return is required to be signed by a Company Secretary and in the absence of a Company Secretary by a PCS.

Provided that in case of in relation to One Person Company and Small Company, the annual return shall be signed by the company secretary, or where there is no company secretary, by the director of the Company.

As per Section 2 (85) of the Act, 2013

‘‘small company’’ means a company, other than a public company,—

(i) paid-up share capital of which does not exceed fifty lakh rupees or such higher amount as may be prescribed which shall not be more than five crore rupees; or

(ii) turnover of which as per its last profit and loss account does not exceed two crore rupees or such higher amount as may be prescribed which shall not be more than twenty crore rupees:

Provided that nothing in this clause shall apply to—

(A) a holding company or a subsidiary company;

(B) a company registered under section 8; or

(C) a company or body corporate governed by any special Act;

Further, as per draft rule 7.9 (2) the Annual Return, filed by a listed company or a company having paid-up share capital of five crore rupees or more and turnover of twenty five crore rupees or more, needs to be certified by a PCS. The certificate shall be in Form no. 7.8

As per Section 203, every listed company and every other company having a paid-up share capital of five crore rupees or more need to appoint full time Company Secretary (a Key Managerial Personnel as per Section 2(51) of the Act, 2013). Except for section 203, the Act, 2013 does not provide for appointment of full time Company Secretary.

The Act, 2013 further, under Section 204, even mandates Secretarial Audit for a listed company and every public company having a paid-up share capital of one hundred crore rupees or more, which shall be given by a PCS and such report shall be annexed to the Board Report of the Company.

Our Analysis

Based on the above discussions we can classify companies in 5 categories and state the relevant compliance requirements with respect to PCS.

Statistical Analysis

According to the October 2011 statistics from the Department of Company Affairs , there are 11, 63, 136 companies registered in India. Of these, only 24,682 (or 2.12 per cent) have paid-up capital between ` 2 crore and ` 5 crore, and Companies with paid-up capital over ` 5 crore number 23,589 (2.02 per cent).

In other words, a good majority, i.e. 98 per cent, have paid-up capital below ` 5 crore. A whopping 11, 14,865 companies (95.85 per cent) have paid-up capital less than ` 2 crore. Listed companies comprise only 0.6 per cent; the remaining 1.4 per cent are unlisted public or private companies

Further, as per the information gathered from professional colleagues at present there are about 9 lakhs active companies. Out of these, about 7 lakhs companies have a paid up capital of upto ` 50 lakhs which comprises of about only 35000 public companies and the rest are private companies (i.e. a ‘small company’ as discussed above)

So, if we exclude small companies from the abovementioned statistics, we will still have a reasonable figure of companies which will require its Annual Return to be signed by PCS. The reason behind this is that companies with paid up capital of below ` 5 crore were neither required to appoint a Company Secretary under the Act, 1956 nor is it mandatory to appoint under the Act, 2013. Therefore, we presume that these companies will not appoint a Company Secretary in employment. Further considering that there are only around 5800 PCS in the country, each PCS will get to sign a reasonable number of Annual Returns, even if all such companies were to be distributed evenly. So all the practicing professionals surely have a reason to cheer!

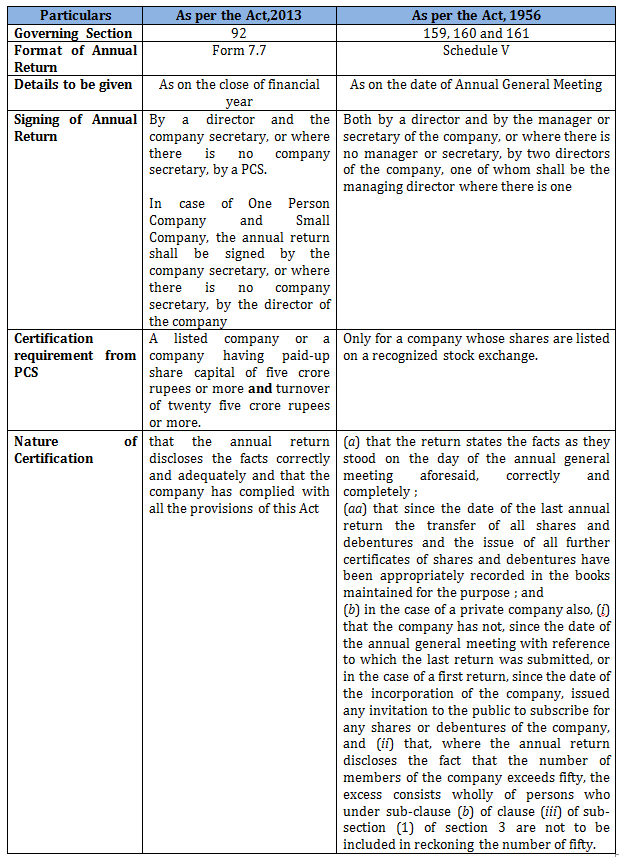

Annual Return under Act, 2013 v/s Annual Return under Act, 1956

The content of Annual Return is very exhaustive as opposed to Schedule V under Act, 1956. Further, the certification is not limited to contents of Annual Return but also covers compliance with all the provisions of the Act. The format of Certificate to be given under the Act (Form 7.8) is very similar to a Compliance Certificate under the Act, 1956. 1956. Apart from this, other particulars such as remunerations, details of KMP, number of board and committee meetings held etc. also has to be certified. Therefore, this certification in itself is wholesome.

Verification v/s Certification

In case of a PCS being a co-signatory to the Annual Return, the PCS will only be verifying the information stated in the Annual Return. However, where the Annual Return requires certification of PCS, the PCS shall not only verify the contents of Annual Return but also certify compliance with provisions of the Act (as specified in Form 7.8).

Section 161 of Act, 1956 required certification of Annual Return only for listed companies. Interestingly, Act, 2013 ha widened the scope and has included Companies with paid up capital of ` 5 crores or more and turnover of ` 25 crores or more within the ambit of PCS certification.

Further, as compared to Compliance Certificate prescribed under section 383A of Act, 1956, Annual Return certification under Act, 2013 is more extensive. Therefore, there is increased responsibility and accountability also with increased role and scope.

Conclusion

From the above discussion and analysis it is very evident that the both the scope and attribute of PCS is about to increase. However, it is to be kept in mind that with more responsibility comes more accountability. Keeping in mind that the certification requirements are by and large very exhaustive and complex, practising company secretaries have to exercise due caution.

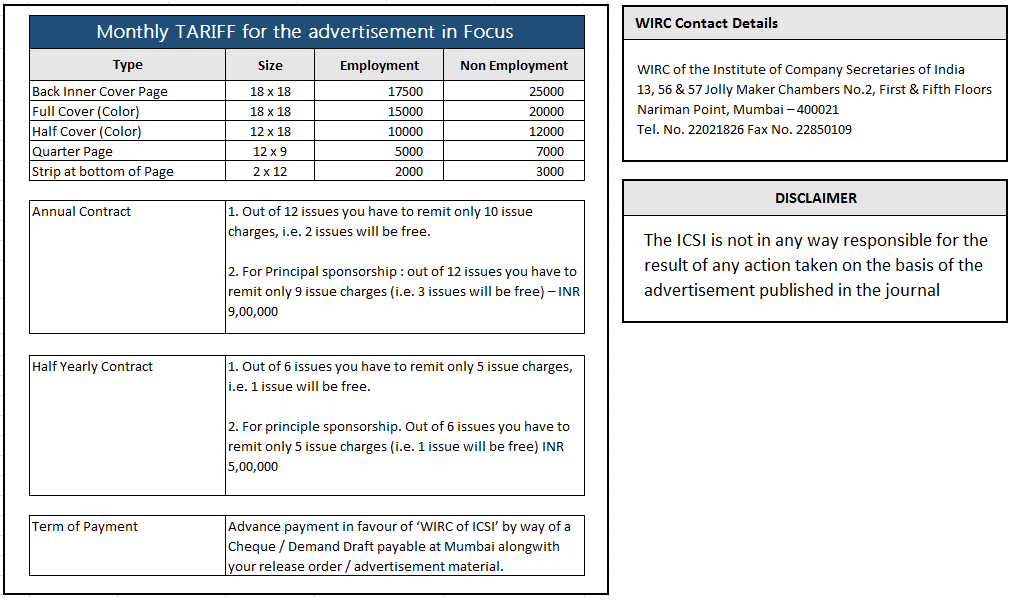

WIRC Advertisements

Case Laws at a Glance

A Bird’s Eye View: Recent judgements on Company Law

1) COMPROMISE AND ARRANGEMENT

1) COMPROMISE AND ARRANGEMENT

Respondent Company was ordered to be wound up. Shareholders proposed revival scheme. Company sought sanction of revival scheme. Over 90 per cent of shareholders, secured creditors and unsecured creditors of Respondent Company approved scheme. Strategic investor also brought money, a part of which was used to pay off some of secured creditors. Remaining creditors conveyed to Court that they accepted terms of payment schedule as proposed. Further, Propounder of scheme filed affidavit assuring payment of future statutory or Government dues. Sanction was to be accorded to proposed scheme. – GUJRAT STATE FINANCIAL SERVICES LTD. V. THAPAR AGRO MILLS LTD. [2013] 120 SCL 46 (DELHI)

2) OPPRESSION AND MISMANAGEMENT

Petitioner Company was holding 24 per cent shares in respondent company. It had two directors on Board of Respondent–Company. Both of them were regular attendants of Board Meetings. Without issuing notice to Petitioners Directors, Respondents removed them on ground of non-attendance of Board Meetings. Thereafter new shares were allotted and share capital was increased. These acts were per se oppressive. To balance equity, opportunity to raise share capital to restore Petitioner-company’s shareholding must be given to Respondents. – DAKSHA INFRA BUILD (P.) LTD. V. ROCHEES RESORTS (INDIA) (P.) LTD. [2013] 119 SCL 309 (CLB - NEW DELHI)

3) NUMBER OF DIRECTORS

A director, unless expressly authorised by board of directors cannot act individually to represent a private limited company in which there has to be minimum two directors in board of directors to exercise powers of company. Respondent-company was family company of ‘M’ Plaintiffs, i.e. ‘S’ and ‘R’, and defendant, i.e. ‘A’ were children of ‘M’. After death of ‘M’ and his wife, ‘A’ became sole director of company and appointed additional directors. Plaintiffs who had equal stake in company filed suit against Respondent and defendant alleging that ‘A’ could not act as sole director and that Plaintiffs were interested in taking control and managing company. After death of two directors out of three directors there could not be any board and therefore, ‘A’ could not function assuming powers of board. For time being Plaintiffs and ‘A’ would constitute board of directors and convene meetings. - SREEJAYA BHATTACHARJEE GODFREY V. SHREEJAYA TEA & INDUTRIES (P.) LTD. [2013] 119 SCL 344 (CAL)

4) APPEAL AGAINST ORDER OF COMPANY LAW BOARD

Appellants cannot be precluded from canvassing other questions of law if they fall within the framework of the questions of law which were in issue before the Company Law Board – section 10F – MANOJ KUMAR KANUNGA V. MARUDHAR POWER (P.) LTD. [2013] 116 CLA 263 (AP)

5) ARRANGEMENT

An application under sections 391 and 392 is not maintainable for recalling an order by which a scheme of arrangement has been sanctioned. – Sections 391 and 392 – CASTRON TECHNOLOGIES LTD. V. CASTRON MINNING LTD. [2013] 116 CLA 322 (CAL)

6) COMPANY LAW BOARD TO CALL MEETING

If requirement of section 257 are not complied with, the Company Law Board will be justified in directing company to call a general meeting under section 257 read with regulation 44 of Company Law Board Regulations, 1991 – WYNN’S BELGIUM NV V. MEKUBA PETROLEUM INDIA (P.) LTD. [2013] 116 CLA 169 (CLB)

7) OPPRESSION / MISMANAGEMENT

Allegation of forgery, etc, made to police are under investigation, it is not proper for the Company Law Board to come to any conclusion as to forgery under section 397/398 read with rule 1 of order 23 of Code of Civil Procedure, 1908 – N VENKATESHWAR RAO V. SHARVANI ENERGY (P.) LTD. [2013] 116 CLA 178 (CLB)

8) TRANSFER OF PLEDGED SHARES

Company is not justified in refusing transfer of pledged shares on untenable grounds – Section 111/111A – GUJRAT STATE FINANCIAL CORPORATION V. PAREKH PLATINUM LTD. [2013] 116 CLA 195 (CLB)

Circulars & Notifications

MINISTRY OF CORPORATE AFFAIRS

1. REGARDING RELAXATION OF LAST DATE AND ADDITIONAL FEE IN FILING OF E-FORM 23C FOR APPOINTMENT OF COST AUDITOR.

General Circular No. 17/2013

Source: www.mca.gov.in

Reference is invited to General Circular No. 14/2013 dated 3rd September,2013 through which the last date of filing and to relax the

additional fee applicable on e-form 23C was extended up to 31st October, 2013 or within 30 days of the commencement of the company’s

financial year to which the appointment relates, whichever is later.

financial year to which the appointment relates, whichever is later.

2. It has now been decided to extend the last date of filing and to relax the additional fee applicable on e-form 23C to 30th November, 2013

or within 30 days of the commencement of the company’s financial year to which the appointment relates, whichever is later.

3. REGARDING CLARIFICATION WITH REGARD TO APPLICABILITY OF PROVISION OF SECTION 372A OF THE COMPANIES ACT, 1956.

General Circular No. 18/2013

Source: www.mca.gov.in

This Ministry has received number of representations consequent upon notifying Section 185 of the Companies Act, 2013 dealing with loans to directors which is corresponding to Section 295 of the Companies Act, 1956. Section 186 of the Companies Act, 2013 is yet to be notified.

It is clarified that Section 372A of the Companies Act, 1956 dealing with inter-corporate loans continue to remain in force till section 186. of the Companies Act, 2013 is notified.

This issues with the approval of competent authority

CUSTOMS

1. REGARDING APPLICABLE CVD ON STEAM COAL IMPORTED FROM INDONESIA UNDER FTA NOTIFICATION NO. 46/2011

2.

Circular No. 41/2013 – Customs

Source: www.cbec.gov.in

I am directed to invite your attention to the above mentioned subject.

3. Under notification No. 12/2012-Customs, dated 17-03-2012 (S. No. 123 of the Table), Steam Coal falling under sub-heading 27011920 attracts basic customs duty (BCD) at 2% and countervailing duty (CVD) at 2%. Steam Coal imported from Indonesia enjoys preferential BCD @ 0% under S. No. 207 of notification No. 46/2011-Customs, dated 1st June 2011 (India-ASEAN FTA). In this connection, a doubt has been raised whether an importer, while availing of the BCD exemption @ 0% under FTA (notification No. 46/2011-Customs), can simultaneously avail of the concessional CVD @ 2% as per notification No.12/2012-Customs, or he has to pay the CVD at 6%, which is the rate of excise duty applicable on Steam Coal when Cenvat facility has been availed of.

4. The matter has been examined by the Ministry. Under the Free Trade Agreement (FTA), the preference / concession is extended only in respect of BCD. All other duties, including CVD are charged as applicable to similar imports from other countries. The CVD on an imported article is levied at a rate equal to the excise duty leviable on a like article, if produced or manufactured in India. However, at times, under a notification issued under section 25(1) of the Customs Act, 1962, CVD is levied at a rate which is lower than the rate of excise duty leviable on the like domestic article.

5. In the present case, the excise duty applicable on Steam Coal is 6%, if CENVAT benefit is availed of and 1% if the CENVAT benefit is not availed of. Normally, Steam Coal will suffer 6% CVD, as the condition of non-availment of cenvat benefit cannot be satisfied in respect of imported goods. However, in the Budget 2013-14, as a conscious policy decision, it was decided to levy 2% CVD both on steam coal and bituminous coal. This is the general applied rate of CVD on all imports of steam coal and bituminous coal regardless of the excise duty leviable on like domestic coal. No such condition has been laid down that an importer cannot avail of this concessional CVD of 2% if he has availed of the concessional BCD on steam coal under another notification.

6. It is therefore clarified that an importer while availing of BCD exemption on steam coal under FTA notification No. 46/2011-Cus can simultaneously avail of concessional CVD at 2% under notification No. 12/2012-Cus.

7. Difficulties, if any, faced in the implementation of above instructions may be brought to the notice of the Ministry at an early date.

REGARDING ENCOURAGING STAKEHOLDER PARTICIPATION IN CUSTOMS FUNCTIONING

Circular No. 42/2013 – Customs

Source: www.cbec.gov.in

The CBEC has a well established practice of involving stakeholders in decision-making and resolving operational issues. This is exemplified by the Permanent Trade Facilitation Committee (PTFCs) in each Custom House, which includes local trade and logistics association as well as Customs Brokers association. These committees typically meet once a month for deliberating issues that impact day to day functioning. All senior departmental officers including Commissioners of Customs attend the meetings.

2. In this regard I am directed to state that noting the efficacy of the PTFCs in resolving local issues the Board is of the view that these are needed to be well attended by the trade bodies. Also, the PTFC meetings should be held at all Customs locations, if not being done so already. This would ensure that local issues of interest to the trade would get resolved quickly thereby furthering the cause of trade facilitation. This would also prevent the escalation of purely local issues to the Department/Board.

3. The Board also notes that possibly, issues could be better resolved at the local level if presented to the Chief Commissioners/Commissioners by the apex trade bodies, who by virtue of membership spread across Custom Houses would have a broader perspective. Hence, it would be fruitful to encourage the apex trade bodies to meet the Chief Commissioners/Commissioners. The apex trade bodies could also attend the PTFCs along with their constituents, who are members of the PTFCs.

4. The Board desires that as a trade facilitation measure aimed at encouraging stakeholder participation and expeditious resolution of local issues (without these being escalated to the Department/Board) the Chief Commissioners should henceforth ensure that:-

(a) The PTFCs are held regularly with minimum of one meeting each per month on a pre-decided date.

(b) Minutes of the PTFC meetings are sent to the Board through DG, Directorate General of Export Promotion on issues having all India implication, if any.

(c) Apex trade bodies are allowed to attend the PTFC meetings along with their local constituents, who are members of the PTFC.

(d) Efforts are made to regularly review the membership of the PTFC with the aim of including all stakeholders in the Customs functioning.

(e) Chief Commissioners/Commissioners are receptive to meeting local and apex trade bodies even outside the framework of the PTFC.

5. Difficulties, if any, faced in the implementation of the instructions may be brought to the notice of the Ministry at an early date.

3. REGARDING EXEMPTION FROM PAYMENT OF SAD TO PARTS, COMPONENTS AND ACCESSORIES ETC. OF MOBILE HANDSETS UNDER NOTIFICATION NO. 21/2012-CUS, DATED 17/03/2012

Circular No. 43/2013 – Customs

Source: www.cbec.gov.in

I am directed to invite your attention to notification No. 21/2012-Cus, dated 17-03-2012 (S. No. 5 of the Table) providing exemption from payment of SAD to parts, components and accessories etc for the manufacture of mobile handsets. The exemption was valid until 31.3.2013 and was subject to actual user condition, that is to say, the importer was required to follow the procedure set out in the Customs (Import of Goods at Concessional Rate of Duty for Manufacture of Excisable Goods) Rules, 1996.

2. It has been reported that after 31.3.2013, manufacturer/importers are claiming exemption from SAD on the said goods under the said notification in terms of S. No. 1 of the Table, which provides exemption from SAD to all goods that are exempt from payment of BCD and CVD. As this S.No. does not stipulate observance of any actual user condition (unlike S. No. 5 of notification No. 21/2012-Cus, which provided exemption subject to actual user condition), a doubt has been raised whether exemption from SAD should be allowed on the said goods.

3. The matter has been examined. Under notification No.21/2012-Cus dated 17.3.2012 (S.No. 1 of the Table), “goods which are exempt from the whole of the duty of customs leviable thereon or in case of which “Free” or “Nil” rates of duty of customs are specified in column (4) under the First Schedule to the Customs Tariff Act, 1975 (51 of 1975) and which are also exempt from the whole of additional duty of customs leviable thereon under sub-section (1) of section 3 of the said Act, or on which no amount of the said additional duties of customs is payable for any reason,” are exempt from SAD. Parts, components and accessories, etc required for the manufacture of mobile handsets are exempt from BCD and CVD under notification No. 12/2012-Cus, dated 17.3.2012 (S.No. 431 of the Table) subject to the condition that the importer follows the procedure set out in the Customs (Import of Goods at Concessional Rate of Duty for Manufacture of Excisable Goods) Rules, 1996. As per these rules, the manufacturer/importer is required to produce before Customs a certificate from the jurisdictional Central Excise authorities as laid down under the said Rules. In view of this, particularly considering that the manufacturer/importer furnishes to the customs authorities the required certificate for availing of the benefit of exemption from BCD and CVD in respect of parts, components, accessories etc imported for the manufacture of mobile handsets, it has been felt that the benefit of exemption from SAD should not be denied in respect of the same goods if claimed under S.No.1 of notification No.21/2012-Customs. The certificate which is valid for claiming exemption from BCD and CVD ought to be taken cognizance of and the benefit of SAD exemption allowed.

4. Accordingly, it is clarified that exemption from SAD under notification No. 21/2012-Customs (S.No. 1 of the Table) may be allowed at the port of import on the basis of registration and the certificate issued by the jurisdictional central excise authorities w.r.t S.No. 431 of notification No. 12/2012-Customs without any requirement of a separate registration/certificate issued under the said Rules w.r.t notification No. 21/2012-Customs, dated 17-3-2012.

5. Difficulties, if any, faced in the implementation of above instructions may be brought to the notice of the Ministry at an early date.

CENTRAL EXCISE

1. REGARDING AMENDMENT OF RULE 8, 9 AND 10 OF THE CENTRAL EXCISE VALUATION (DETERMINATION OF PRICE OF EXCISABLE GOODS) RULES, 2000

Circular No. 975/09/2013-CX

Source: www.cbec.gov.in

I am directed to invite your attention to amendments in rule 8, 9 and 10 of the Central Excise Valuation (Determination of Price of Excisable Goods) Rules, 2000. Under transaction value regime each transaction or removal is required to be assessed independently, as would be clear from the language of section 4 of the Central Excise Act, 1944. Section 4(1) of the Central Excise Act, 1944 reads as –

Section 4 – Valuation of excisable goods for purposes of charging of duty of excise - (1) Where under this Act, the duty of excise is chargeable on any excisable goods with reference to their value, then, on each removal of the goods, such value shall –

…………………………………

2) Rules 8, 9 and 10 of the Central Excise Valuation Rules, 2000 dealing with determination of assessable value in case of captive consumption and sale to related person have been amended vide notification no. 14/2013 – Central Excise (N.T.) dated 22.11.2013 to clearly state that these rules apply irrespective of whether the whole or a part of the clearances of manufactured goods are covered by the circumstances given in these rules. Each clearance is required to be assessed according to section 4(1)(a) or the relevant rule dealing with the circumstances of clearance of the goods, as the case may be.

3) For example, if an assessee clears his goods in such a way that first removal of goods is to an independent buyers, some goods are captively consumed, second removal is to such a related person who is covered under rule 9 and third removal is to a person who is covered under rule 10, then the first removal should assessed under section 4(1)(a), captively consumed goods should be assessed under rule 8, second removal should be assessed under rule 9 and third removal should be assessed under rule 10 of these rules. It may be noted that Central Excise Valuation (Determination of Price of Excisable Goods) Rules, 2000 are not required to be followed sequentially. Each of these rules provide for arriving at the assessable value of goods under different contingencies as noted by Hon’ble Supreme Court at paragraph 70 in case of Commissioner of Central Excise, Mumbai vs M/s FIAT India Pvt Ltd [2012 (283) ELT 161 or 2012-TIOL-58-SC-CX].

4) Serial no. 5, 12 and 14 of the Circular no. 643/34/2002-CX dated 1-7-2002 are deleted in view of the amendments in the Central Excise Valuation (Determination of Price of Excisable Goods) Rules, 2000, as these amendments address the issues on which these clarifications were issued. The amended rules and accordingly this circular shall apply with effect from 1st December, 2013.

SERVICE TAX

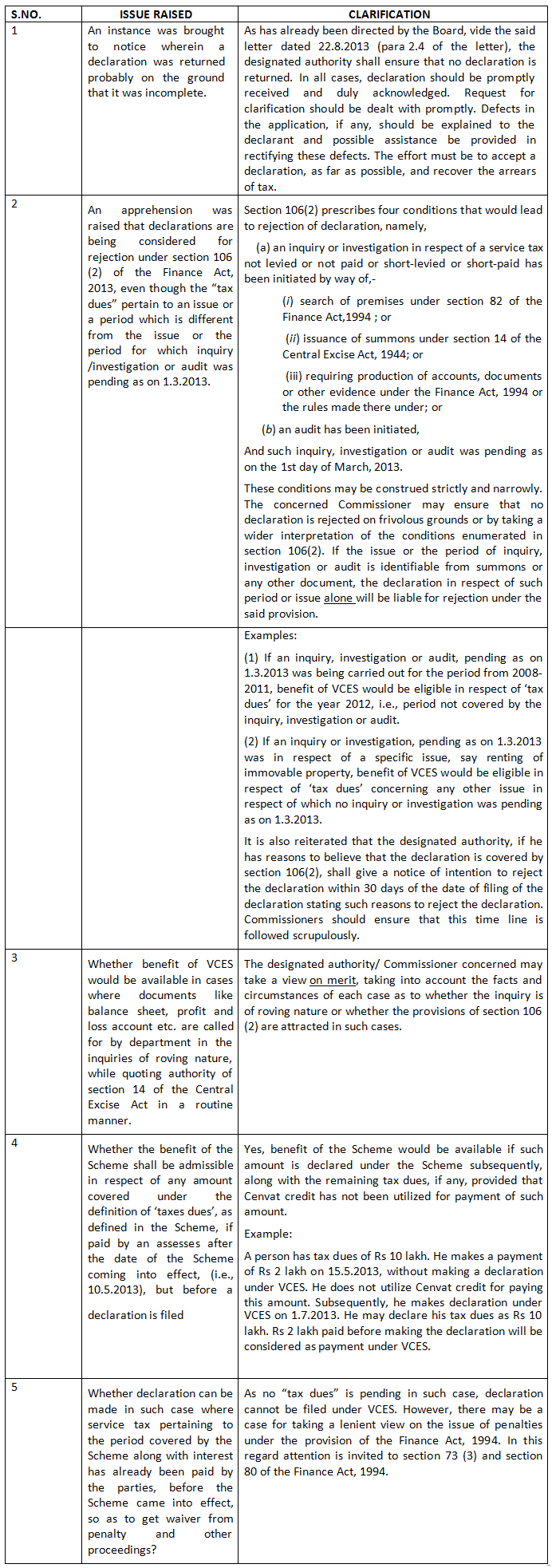

1. REGARDING THE SERVICE TAX VOLUNTARY COMPLIANCE ENCOURAGEMENT SCHEME

Circular No. 174/9/2013 – ST

Source: www.servicetax.gov.in

The Service Tax Voluntary Compliance Encouragement Scheme (VCES) has come into effect from 10.5.2013. Most of the issues raised with reference to the Scheme have been clarified by the Board vide circular Nos. 169/4/2013-ST, dated 13.5.2013 and No. 170/5/2013-ST, dated 8.8.2013. These clarifications have also been released in the form of FAQs. Attention is also invited to letter F. No. 137/50/2013-ST, dated 22.8.2013 as regards the action to be taken by the field formations for effective implementation of the Scheme. A number of interactive sessions have also been held at various places to ascertain and address the concerns of trade on any aspect of the Scheme.

2. In the recently held interactive sessions at Chennai, Delhi and Mumbai, which were chaired by the Hon’ble Finance Minister, the trade had raised certain queries and also expressed some apprehensions. Most of these issues have already been clarified in the aforementioned circulars/FAQs. Certain issues raised in these interactive sessions, which have not been specifically clarified hitherto or clarified adequately, are discussed and clarified as below.

3. Trade Notice/Public Notice may be issued to the field formations and tax payers. Please acknowledge receipt of this Circular. Hindi version follows.

Monthly Compliance Calendar

Smile Please / Cartoon

WIRC News

33rd Management Skills Orientation Program (MSOP) of ICSI-WIRC

ICSI-WIRC organized its 33rd Management Skills Orientation Program from Friday, November 08, 2013 to Tuesday, November 26, 2013.

Shri Rasik Somaiya, Chairman, Span Capital Services Pvt. Ltd. delivered the inaugural address. He spoke on the significance of inter Personal relationship and also emphasized to the participants to perform ‘out of box’. He also elaborated the role of various regulatory bodies especially SEBI in context of various scams in the corporate sector.

The 15 days of MSOP was a proper blend of Soft Skills & Technical Sessions. Topics like Communication & Presentation Skills, Professional Etiquettes, Emotional Intelligence, Stress Management, Leadership Mantras & Team building, FEMA, Intellectual Property Rights, IPO with case studies, Basics of SARFAESI ACT-2002, Loan Documentation, New Takeover Code, New Companies Act etc were covered during MSOP.

The Project presentations was held on Monday November 25, 2013. The group comprising of Mr. Amey Borkar, Ms. Melisa Alva, Ms. Nisha Shetty, Ms. Ketki Bhogle Ms. Sonam Jain whose Project was adjudged as “Best Project Group” . The topic of the best project was “Indian Foreign Direct Investments strategies in Telecom Industry ( Case study of a Public & Private Industry)”& Mr. Siddhartha Shevde was adjudged as the “Best Presenter”.

A visit was arranged to the Link Intime India Pvt. Ltd. where the participants got good exposure of Transfer of Shares.

The Valedictory session of the MSOP was held on Tuesday November 26, 2013. Shri Shailesh Rajadhyaksha, Advisor, Tata Capital Ltd. was the Chief Guest. He shared his experience with the participants & distributed the course completion certificates.

Chapter News

Media Coverage

Chapter - Photo Gallery

WIRC - Photo Gallery

Career Opportunities & Vacancies

Editorial Policy

A : “FOCUS” published monthly as a magazine aims to be a forum for members of the Western India Regional Council of the Institute of Company Secretaries of India ( WIRC of ICSI) for;a. DISSEMATING information,

b. COMMUNICATING developments affecting the Institute and its members in particular and the CS profession in general,

c. ARTICULATING issues of contemporary concern to the members of the profession.

d. CEMENTING and DEVELOPING relationships across membership by promoting discussion and dialogue on professional issues.

e. DISCUSSING and DEBATING issues particularly of public interest, which could be served by the CS profession.

f. FACILITATING Members of the profession to share their views on matters of professional interest by way of articles and write-ups.

B : The WIRC of ICSI recognizes the fact that;

a. There is a growing emphasis on the globalization of the CS profession;

b. There is an imminent need to position the profession in a business context which transcends the traditional and specific CS applications.

c. The Institute members increasingly will work across the globle and in global context.

C : Given this background the WIRC of ICSI strongly encourage contributions from the following groups of professionals;

a. Members of other Professional bodies across the globe

b. Regulators and Government officials

c. Professionals from allied professions

d. Academia

e. Professionals from other disciplines whose views are of interest to the CS profession

f. Business leaders

D : The magazine also seeks to keep members updated on the activities of the Institute including events on the various practice areas and the various professional development programs on the anvil.

E : The WIRC of ICSI while encouraging stakeholders as in Section C to Contribute to the Magazine , it makes it clear that responsibility for authenticity of the contents or opinions expressed in any material published in the Magazine is solely of its author and the WIRC of ICSI, council members, any of its editors or members of Editorial Team & Advisory Board, the staff working on it or “FOCUS” is in no way holds responsibility there for. In respect of the advertisements, the advertisers are solely responsible for contents of such advertisements and implications of the same.

F : Finally and most importantly WIRC of ICSI strongly believes that the magazine must play its part in motivating students to grow fast as Members of tomorrow to be capable of serving the Legal & Compliance area within ever demanding customer expectations.

Tariff/Disclaimer